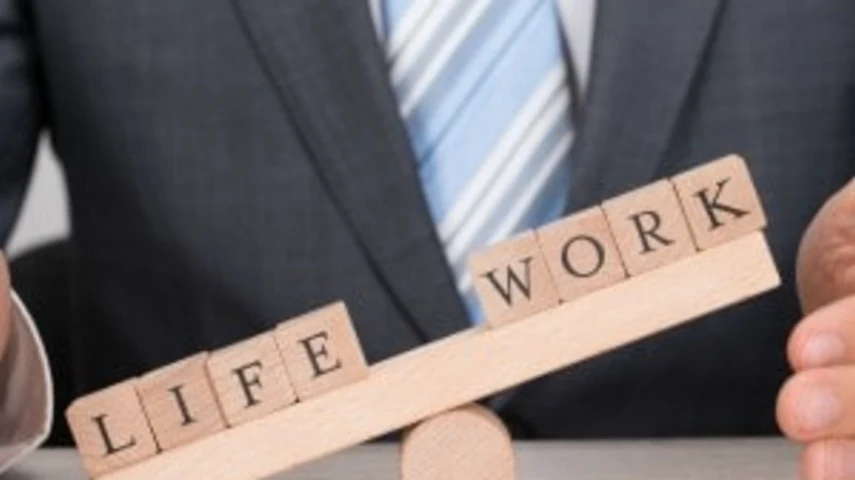

Work-life balance a challenge in finserv

Accounting and financial services professionals are struggling to manage the work-life balance even as confidence remains high among their firms, Macquarie found.

The firm's 2015/16 Accounting and Financial Services (AFS) Benchmarking Report found that while 83 per cent of the 355 people surveyed were confident about their future business prospects, many found it a challenge to balance work and their personal lives.

Division director for Macquarie Wealth Management, David Clatworthy, said financial services principals and partners found it challenging to prioritise their own goals while simultaneously growing the business, and this was the case across all firms, no matter the size.

"For example, 45 per cent of leaders at firms earning more than $2 million per year in revenue reported not having enough time with their family as a major concern, compared to 35 per cent of smaller businesses," Clatworthy said.

However, he noted that the highest performing firms more actively used their resources to help manage the balance.

"Ultimately, the principals and partners of the highest performing firms are less likely to see work-life balance and fatigue as solely personal challenges, and are more willing to leverage their firm's resources in order to find more time for the things that matter — time with family, for themselves and on their business," Clatworthy said.

Almost half of all owners of large firms (48 per cent) said they did not have enough time to do what they wished for their business, while 44 per cent of small firm owners said the same.

"Greater business efficiencies and internal cohesion is needed to help win back more personal time," Clatworthy said.

AUTHOR

Malavika Santhebennur

Recommended for you

The Financial Advice Association Australia has appealed to licensees to urgently update their FAR records as hundreds of advisers are set to depart by the end of the year.

Demand for robo-advice tools is rising, a report has shown, but this is occurring simultaneously with rising demand for professional face-to-face advice.

ASIC has released the results of the latest financial adviser exam, held in November 2025.

Winners have been announced for this year's ifa Excellence Awards, hosted by Money Management's sister brand ifa.